If you’ve felt like you are running at 100 miles an hour on a financial treadmill—working harder than ever but standing completely still—you are not alone. Tonight, we are stripping away the anxiety and the noise. We aren't here to lecture you; we are here to give you an operational playbook to stop playing defense, break the cycle, and take back control of your capital. Let’s get to work.“

It’s Not Just a Low-Income Issue

A critical misconception is that this cycle only affects those with low wages. In reality, "lifestyle creep" and high debt loads trap high earners in the exact same loop. Whether someone makes $40,000 or $250,000, if their fixed commitments mirror their take-home pay, they are equally vulnerable to a sudden disruption in income.

As promised, I have attached the full slide presentation deck to this email. Below is a quick recap of the core takeaways we covered.

THE DOMINO EFFECT: WHAT REALLY HAPPENS WHEN YOU MAX OUT YOUR CREDIT

The Domino Effect: What Really Happens When You Max Out Your Credit

It is one of the most pervasive mental traps in modern personal and business finance: you open an app, log into your dashboard, and see a crisp, clean number staring back at you.

“Credit Limit: $25,000. Available Credit: $25,000.”

To the untrained eye, that screen represents $25,000 of emergency backup cash, a financial safety net, or a pool of capital waiting to fund your next big move. But this perspective is a dangerous mirage. It relies on a fundamental misunderstanding of financial engineering known as The Illusion of "Available" Capital.

When you treat a credit limit as if it were cash in the bank, you set yourself up for a rude awakening. The moment you push a credit card to 100% utilization, you pull a lever that triggers a silent, destructive, and deeply interconnected chain reaction.

This is the financial Domino Effect—and here is what really happens behind closed doors when you max out your credit.

Domino 1: Shattering the Illusion of "Available" Capital

To understand why the dominoes fall, you must first shatter the illusion.

Available Capital is wealth you explicitly own. It is the liquid cash sitting in your checking account, your business reserves, or your money market funds. When you deploy your own capital, your asset balance changes, but your structural risk remains zero. You owe nothing to anyone, and your financial infrastructure remains entirely under your control.

Credit, on the other hand, is a tool for leverage. It is not your money; it belongs entirely to a financial institution.

When you confuse the two and max out a credit card, you aren’t just spending money—you are radically transforming your balance sheet from an asset-focused foundation to a liability-heavy cage. You have traded your freedom for an institutional debt obligation, and the banking algorithms will immediately punish you for it.

Domino 2: The FICO Score Cliff-Dive

The moment your credit card statement closes at 100% utilization, the first visible domino falls: your credit score takes a massive hit.

Under the FICO scoring model, Amounts Owed (which is heavily dictated by your debt-to-limit utilization ratio) commands a massive 30% of your total score. The algorithm looks at your utilization in two ways: across all your cards combined, and on individual cards.

You might think, "I have a total of $100,000 in credit across five cards, so maxing out this one $10,000 card means my overall utilization is only 10%. I'm safe." The reality is: you aren't. The FICO algorithm severely penalizes individual maxed-out cards. Pushing a single card to its ceiling flags you as a high-risk borrower. Almost overnight, your score can drop anywhere from 30 to over 100 points, instantly freezing your institutional loan readiness for mortgages, commercial loans, or auto financing.

Domino 3: The Trap of "Balance Chasing"

Let's say you realize your mistake. Your credit score has dropped, your available credit is at zero, and you decide to do the responsible thing. You scrape together $3,000 in cash and make a major payment to give yourself some breathing room. You expect your available credit to bounce back to $3,000.

Instead, you fall victim to an institutional trap known as Balance Chasing.

When credit card issuers see a borrower max out a card, their internal risk algorithms go on high alert. They assume you are facing financial distress. To mitigate their own exposure, the moment your $3,000 payment clears, the bank automatically slashes your overall credit limit by that exact same amount.

Your balance drops from $10,000 to $7,000—but your credit limit is lowered to $7,000, too.

Mechanically, you are still at 100% utilization. The bank has swallowed your cash, wiped out your liquidity, left you with zero available credit, and kept your credit score pinned to the floor.

Domino 4: Cross-Issuer Contagion

If you think the damage is contained to the one card you maxed out, you are underestimating how interconnected the modern banking system truly is.

Major credit card companies do not just look at your credit report when you apply for a card. They run automated "soft pulls" on your credit profile every single month to audit your financial health.

Imagine you max out your card with Bank A. Within 30 days, Bank B—where you hold a completely separate card with a pristine $20,000 limit that you rarely use—runs its monthly soft check. They see the massive red flag on your report from Bank A.

Bank B doesn't care that you've always paid them on time. They only see that you are exhibiting high-risk borrowing behavior elsewhere. To protect themselves, Bank B preemptively slashes your credit limit or freezes your account entirely. This is Cross-Issuer Contagion—a financial domino effect where a fire in one corner of your portfolio burns down your entire credit architecture.

Domino 5: The Interest Rate Spiral

As your credit limits vanish and your utilization remains maxed out, the final domino drops: the cost of your debt skyrockets.

Many credit card agreements include clauses that allow lenders to adjust your Annual Percentage Rate (APR) based on your risk profile. If you trigger universal risk flags across the bureaus, your interest rate can instantly spiral from a standard 15% to a punishing penalty rate of 29.99%.

When you combine a 30% interest rate with a credit limit that is being aggressively chased downward by the bank, you enter a compounding debt spiral. Your hard-earned cash flow is entirely consumed by servicing minimum payments, leaving you with no capital left to invest or scale your wealth.

How to Stop the Dominoes: The Recovery Plan

If you find yourself caught in this cycle, traditional financial advice like "just spend less" isn't enough; you have to outsmart the banking algorithms. You can halt the domino effect by executing three tactical adjustments:

Deploy the Micropayment Strategy: Credit bureaus don't record your balance on your due date; they take a snapshot on your Statement Closing Date (20–25 days before your payment is due). Make weekly or bi-weekly payments so your balance is reported as low as possible to FICO.

Isolate individual Maxed Cards: Don't spread your extra cash evenly across your debts. Focus entirely on pushing the card closest to 100% capacity down below 50%, and eventually below 30%. This clears the individual max-out flag and yields the fastest credit score rebound.

Dilute Your Risk (The Ceiling Strategy): Log into your accounts that are in excellent standing with low balances and request a credit limit increase. As long as it is a soft inquiry (which carries no credit score penalty), an increased limit expands your overall credit ceiling, instantly diluting your utilization percentage without costing you a single dollar.

The Bottom Line

Credit is a powerful psychological and operational tool. When used surgically, it provides immense leverage to scale your life and business. But the moment you buy into the illusion of credit as "available capital," the institutional machinery will turn against you.

Protect your infrastructure, respect the algorithms, and never let the first domino fall.

INVESTING 101: FINANCIAL READINESS AND INVESTMENT ACTION

Here are the 10 essential steps for a beginner to build wealth, culminating in Making Your First Trade.

The process of building wealth is divided into two phases: Financial Readiness (Steps 1-5) and Investment Action (Steps 6-10).

WEBINAR SLIDES

The Arc of Ambition: Jonas Oware and the Yale Blue

The squeak of Jonas Oware’s size 16 sneakers was a constant soundtrack to life at Long Beach Poly High. At a statuesque six feet, nine inches, he dominated the Jackrabbits’ court, his wingspan a defensive nightmare, his vertical leap an exclamation point on every alley-oop. He was a star, the kind of talent that had major Division I coaches from across the country calling the Poly offices weekly.

But today, the loudest sound was the gentle thump of an acceptance packet hitting the counseling desk.

Jonas folded his massive frame into the surprisingly small chair across from Ms. Chen, his college counselor. On the outside, he was all long, coiled muscle; inside, his mind was racing, analyzing probabilities like a complex offensive set. He wasn't nervous about playing basketball—that was instinct. He was nervous about committing to his future.

"Jonas," Ms. Chen said, pushing the Yale envelope toward him, "they didn't just want the 6'9" center who averages a double-double. They wanted the young man who placed top-ten in the state Science Olympiad, who aced AP Calc, and who wrote a brilliant essay on the economics of coastal erosion.“

He took the thick envelope. The air in the quiet office was a world away from the humid intensity of the gym. For years, people had assumed his path: a Power Five conference, a one-and-done year, and the NBA draft. But Jonas—the son of two educators—saw basketball as a means, not the end. He was driven by structural engineering, a field that demanded the same precision and foresight he used to read a pick-and-roll.

He tore the seal. The letter confirmed the news he’d already felt deep down: he had been admitted to Yale University. The commitment was official, a handshake deal that honored his dedication to both the hoop and the history books.

The reaction at Poly was immediate and immense.

Coach Lewis, a hard-nosed Poly legend, pulled Jonas aside after practice. “Look, kid, I knew you could go to the NBA one day. But going to Yale? That lasts longer than any career. You redefined what a student-athlete is for every single kid who walks into this gym.”

The news sent a ripple through the national recruiting circuit. A 6'9" academic powerhouse choosing the Ivy League over the siren call of a major athletic scholarship was rare. Jonas hadn’t gone for the flash; he’d chosen the foundation.

"I love basketball," Jonas told a local reporter, standing under the bright lights of the Poly gymnasium where he'd spent thousands of hours. "But Yale offers something deeper—a chance to learn alongside the best minds in the world, to challenge myself structurally, intellectually, and ethically. The court gave me discipline, but the classroom gives me purpose.“

His commitment became a rallying cry for the school, a perfect symbol of the Poly spirit—unmatched athleticism paired with rigorous academic pursuit.

As the season wrapped, Jonas stood in the gym, feeling the familiar squeak of his sneakers on the polished wood. The court had been his proving ground, a place where his height was his advantage. But soon, he would trade the iconic green and yellow of the Jackrabbits for the historic blue of Yale.

Jonas Oware, 6'9", star athlete and future engineer, had built his own launchpad right there at Long Beach Poly, one perfect jump shot and one perfectly reasoned essay at a time. The echoes in the halls weren't just the bounce of the ball; they were the sound of possibility.

By Marie Deary, Wealth Management Financial Advisors

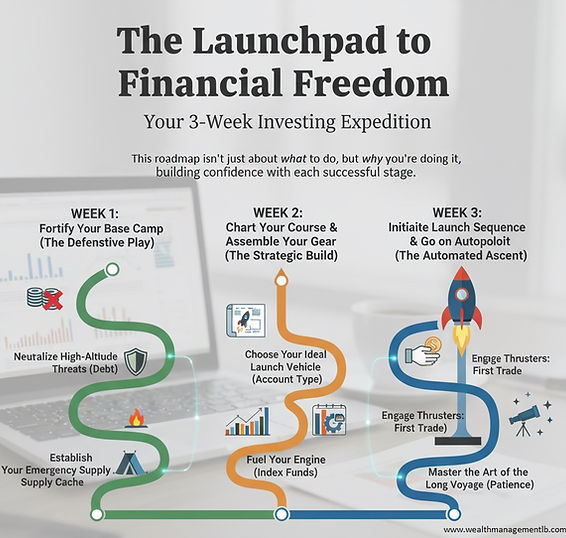

BUILDING WEALTH, INVESTING 101 FOR BEGINNERS: The Launchpad to Financial Freedom

By Marie Deary, Wealth Management Financial Advisors

Investing isn't a secret held by the wealthy; it's a disciplined process anyone can follow. The complexity that overwhelms beginners is often unnecessary. Our "Launchpad to Financial Freedom" breaks the journey into three manageable weeks, ensuring you build confidence, not confusion.

This roadmap isn't just about what to buy; it's about how to build a system that works, balancing financial defense and offense.

🛡️ WEEK 1: Fortify Your Base Camp (The Defensive Play)

Theme: "Build Your Unshakeable Launchpad."

You can't embark on a long journey without securing your starting point. Week 1 is the most critical: eliminating vulnerabilities that could force you to sell investments prematurely. This phase is your financial defense.

Expedition 1: Map Your Financial Terrain (The Money Audit)

Before you invest, you must know exactly what you have available.

-

Action: Conduct a 30-day "Money Audit." Track every dollar in and out using a simple spreadsheet or budgeting app.

-

Outcome: You will discover your true "Investment Surplus"—the precise, reliable amount of money you can commit to investing each month without stress. This surplus is the fuel for your future investment machine.

Expedition 2: Neutralize High-Altitude Threats (High-Interest Debt)

High-interest debt is an invisible drag chute on your finances.

-

Action: Aggressively pay off all debt with an APR (Annual Percentage Rate) over 8–10% (e.g., credit cards, payday loans).

-

The Unique Angle: This isn't just paying bills; it's a guaranteed return far greater than any investment could promise. Eliminate the guaranteed loss first.

Expedition 3: Establish Your Emergency Supply Cache

Your cash reserve is your Investment Protection Shield.

-

Action: Save 3 to 6 months of essential living expenses in a High-Yield Savings Account (HYSA).

-

Purpose: This "Financial Oxygen Tank" ensures that if life throws a curveball (job loss, medical bill), you don't have to sell your investments at a loss. It buys you time and stability.

📈WEEK 2: Chart Your Course & Assemble Your Gear (The Strategic Build)

Week 2 is where you choose your destination, select the right vehicle, and pick your fuel. This is your investment offense.

Expedition 1: Define Your Destination & Risk Tolerance

-

Action: Articulate your goal (e.g., retirement in 30 years). Your time horizon is key: the longer you have, the more market fluctuations you can tolerate.

-

Outcome: Determine your Asset Allocation Map—how much you'll commit to growth assets (stocks) versus stability assets (bonds).

Expedition 2: Choose Your Ideal Launch Vehicle

-

Action: Open a tax-advantaged retirement account first. Choose between a Roth IRA (invest with after-tax money, withdraw tax-free later) or a Traditional IRA/401(k) (upfront tax deduction, tax-deferred growth).

-

Why Tax Advantage? These accounts are "tax-free spaceships" that let your money compound exponentially faster than a regular brokerage account.

Expedition 3: Fuel Your Engine with the Right Blend (Index Funds)

-

Action: Select 1–3 low-cost, broad-market index funds or ETFs (e.g., a Total U.S. Stock Market fund or an S&P 500 fund).

-

The Unique Angle: These are your "Automatic Diversifiers." You are buying a tiny piece of hundreds of companies, which dramatically lowers your risk and ensures you capture the overall growth of the economy. Look for funds with minimal fees (low expense ratios).

➡️ WEEK 3: Initiate Launch Sequence & Go on Autopilot (The Automated Ascent)

This final week is about execution, automation, and long-term discipline.

Expedition 1: Engage Thrusters: Make Your First Trade

-

Action: Fund your new account with your first Investment Surplus and execute your very first purchase of your selected index fund.

-

Significance: Making the first trade is the psychological barrier. You are now officially an investor.

Expedition 2: Activate Autopilot (Dollar-Cost Averaging)

-

Action: Set up Dollar-Cost Averaging (DCA): schedule an automatic, recurring transfer and investment from your bank account to your index fund.

-

Why Automation? DCA removes emotion. You consistently buy shares whether the market is up or down, ensuring you achieve a low average purchase price over time. You are building a "set it and forget it" system.

Expedition 3: Master the Art of the Long Voyage (Patience)

-

Action: Commit to not checking your balance daily. Focus on continuing to fuel your system (DCA).

-

Final Perspective: Success is measured in decades, not days. Volatility is normal. Your job now is to stay the course and let compound interest—the greatest force in finance—do the heavy lifting.

MASTERING YOUR 5 CORE FINANCIAL DOCUMENTS

By Marie Deary, Wealth Management Financial Advisors

Create a Rolling 13-Week Forecast: Don't just look month-to-month. A 13-week (quarterly) rolling forecast is ideal for catching short-term dips. List all expected cash coming in (invoices, loans) and cash going out (payroll, rent, supplier payments) week by week.

Be Realistic with Receivables: Just because an invoice is sent doesn't mean the cash is in the bank. Only forecast cash in when you realistically expect the payment to land.

Identify "Cash Crunches": The forecast will highlight weeks where outgoing cash exceeds incoming cash. This gives you time to adjust, perhaps by delaying a non-essential purchase or proactively chasing a large outstanding invoice.

2. Accelerate Cash Inflow (Get Paid Faster!)

The faster money moves from your customer's pocket to your bank account, the healthier your business.

Optimize Invoicing: Invoice immediately upon service completion or product delivery. Delaying an invoice by a day is delaying payment by a day.

Offer Early Payment Discounts: A small 1-2% discount for payment within 10 days can encourage clients to pay quickly, even if your standard terms are 30 days.

Tighten Payment Terms: If industry standards allow, move from Net 45 or Net 30 to Net 15. Clearly communicate these terms upfront.

Embrace Digital Payments: Make it as easy as possible to pay you. Use online payment platforms (like Stripe, PayPal, or specialized accounting software integrations) that allow for instant credit card or electronic transfers.

3. Control Cash Outflow (Spend Wisely)

Managing what goes out is just as critical as managing what comes in.

Negotiate Favorable Payment Terms: Just as you want to be paid quickly, try to negotiate longer payment terms with your suppliers (e.g., Net 45 instead of Net 30), effectively using their money to manage your short-term needs.

Be Smart About Inventory: Don't tie up capital in excess inventory. Use the "just-in-time" principle where possible, ordering only what you need to meet current demand. Excess stock is just cash sitting on a shelf.

Scrutinize Every Subscription: Small, recurring software subscriptions, utility fees, and services can drain a significant amount of cash over a year. Audit these quarterly and cancel anything you don't use regularly.

Invest vs. Expense: For large equipment or software, evaluate whether an outright purchase is better than leasing or subscribing. Sometimes, spreading the cost (leasing) can preserve critical working capital.

4. Create a Cash Cushion (The Emergency Fund)

Unexpected expenses—a broken piece of equipment, a slow sales month, or an overdue tax bill—can be devastating without a reserve.

Set a Target: Aim to have enough cash in reserve to cover 1 to 3 months of operating expenses. This acts as your business's financial buffer.

Automate Savings: Treat your cash reserve like a recurring bill. Automatically transfer a percentage of your weekly or monthly revenue into a separate, easily accessible savings account dedicated solely to this cushion.

The Takeaway

Cash flow management isn't just about accounting; it's about making proactive, strategic business decisions. When you understand your cash position today and predict it for tomorrow, you move from reacting to financial pressures to proactively steering your business toward sustainable profitability and true success.

Take charge of your cash flow—it’s the key to owning your business future.

WEBINAR SLIDES

1. Master the Forecast, Not Just the PastA Profit & Loss (P&L) statement tells you where you’ve been, but a cash flow forecast tells you where you’re going. This is your most powerful tool.

As a small business owner, you wear many hats – marketer, salesperson, accountant, innovator, and often, chief coffee maker. The journey is exhilarating, but it can also be overwhelming. So, what separates the businesses that merely survive from those that truly thrive?

It boils down to a solid foundation built upon four interconnected pillars. Forget the quick fixes and shiny new trends for a moment, and let’s focus on the timeless principles that form the Small Business Success Blueprint.

Click here to read more

WEBINAR SLIDES

SMALL BUSINESS SUCCESS BLUEPRINT

By Marie Deary, Wealth Management Financial Advisors

TO SUCCEED, WHAT EVERY SMALL BUSINESS OWNER NEEDS TO KNOW

By Marie Deary, Wealth Management Financial Advisors

Unlock the essential knowledge to drive real success in your small business. This power-packed webinar cuts through the noise to deliver the non-negotiable fundamentals every owner must master, from optimizing cash flow and attracting ideal customers to effective scaling strategies and leveraging key technology.

Stop guessing and start knowing the critical steps and common pitfalls. Invest just one hour to gain the clarity and actionable insights that directly translate into sustained growth, stability, and profitability. Don't just run your business—learn how to make it thrive.

A New Chapter of Hope: Beyond the Ballot Box

By Marie Deary, Wealth Management Financial Advisors

Last year, the political landscape felt promising, a feeling many shared across the country. But the election cycle unfolded in a way no one could have predicted. The late entry of a new Democratic nominee, coupled with the political punditry of commentators like Stephen A. Smith who declared the race "doomed," created a whirlwind of uncertainty.

107 Days and the Aftermath

Click here to read more

The October 15 deadline is for most individual taxpayers who filed Form 4868, the "Application for Automatic Extension of Time to File U.S. Individual Income Tax Return." This group includes employees, self-employed individuals, and retirees. It also applies to certain business entities, such as C corporations, that filed for an extension.

Unlike individuals who generally share an April 15 deadline, businesses have staggered original and extended due dates based on their entity type. All dates below are for the 2024 tax year and apply to calendar-year filers.

Click here to read

WEBINAR SLIDES

Beyond Banks and SBA: Navigating the

Diverse Landscape of Small Business Funding

By Marie Deary, Wealth Management Financial Advisors

The entrepreneurial spirit thrives on innovation, passion, and often, a critical injection of capital. For decades, the traditional avenues of bank loans and Small Business Administration (SBA) programs have been the go-to for small business owners seeking funding. While these remain vital resources, the financial landscape has evolved dramatically, offering a rich tapestry of alternative options that cater to diverse needs, risk profiles, and growth aspirations. This chapter delves into the multifaceted world of small business funding, exploring avenues beyond conventional banking to equip entrepreneurs with a comprehensive understanding of their choices.

Click here to read

WEBINAR SLIDES

Navigating the Path to Growth: A Guide to Traditional Funding for Your Small Business

By Marie Deary, Wealth Management Financial Advisors

Is your small business feeling the squeeze of limited capital, holding back your grand plans for expansion, innovation, or simply smoother operations? You're not alone. Many entrepreneurs dream big but find themselves hitting a financial wall. What's often overlooked is that the bridge across that wall is built not just with a great idea, but with sound financial records – especially your business taxes.

Click here to read

WEBINAR SLIDES

THE 5 C'S OF CREDIT:

A LENDER'S EVALUATION FRAMEWORK

By Marie Deary, Wealth Management Financial Advisors

The "5 C's of Credit" is a time-tested framework used by lenders to evaluate the creditworthiness of a borrower. This system provides a comprehensive view of a borrower's ability to repay a loan, helping the lender assess the level of risk involved.

Click here to read

The Financial Compass: 5 Key Financial Documents Every Business Owner and Nonprofit Leader Needs

By Marie Deary, Wealth Management Financial Advisors

Whether you’re selling products, offering a service, or running a mission-driven organization, the language of finance is universal. It’s the language of health, stability, and growth. Yet for many leaders, the core financial documents can feel like a foreign language, filled with jargon and complex numbers.

The truth is, these documents are not just for accountants. They are your most powerful tools for making informed decisions, demonstrating credibility to stakeholders, and steering your organization toward a secure and prosperous future.

Here are the five key financial documents you need to master, with a breakdown for both for-profit businesses and nonprofits.

Click here to read

Click here to download a free copy of the presentation slides.

UNDERSTANDING YOUR ADJUSTED GROSS INCOME (AGI) AND WHY IT MATTERS

By Marie Deary, Wealth Management Financial Advisors

Understanding your Adjusted Gross Income (AGI) isn't just for tax season. It's a foundational number that can have a significant impact on your financial life, both now and in the future. Here are 10 key reasons why knowing your AGI—and whether it's high or low—matters.

Click here to download your free presentation slides.

10 KEY STRATEGIC APPROACHES FOR MASTERING SMALL BUSINESS AND INDIVIDUAL TAXES

By Marie Deary, Wealth Management Financial Advisors

Using legal tax strategies to minimize tax liability is a key part of financial planning for both individuals and businesses. It's not about avoiding taxes illegally, but rather taking advantage of the deductions, credits, and tax-advantaged accounts that are available under the law.

Click here to download

your free presentation slides.

THE INDISPENSABLE ROLE OF TAX PLANNING AND STRATEGIES

By Marie Deary, Wealth Management Financial Advisors

In the intricate world of finance, taxes are an undeniable reality for everyone. However, for African American individuals and small business owners, the strategic management of taxes holds a particularly profound significance.

Click here to read now

YOUR LLC: A WEALTH-BUILDING MACHINE – AND HOW TO KEEP IT RUNNING SMOOTHLY IN CALIFORNIA

By Marie Deary, Wealth Management Financial Advisor

As Wealth Management Financial Advisors, we don't just talk about investments; we talk about building wealth sustainably. For many of our clients, their Limited Liability Company (LLC) isn't just a business entity – it's a powerful wealth-building machine.

Click here to read now

INSIGHT FROM MARIE DEARY OF WEALTH MANAGEMENT FINANCIAL ADVISORS:

POSITIVE CASH FLOW – THE LIFEBLOOD OF YOUR BUSINESS, ESPECIALLY FOR BLACK OWNERS

Click here to read now

SO, YOU WANT TO START A NONPROFIT: INSIGHTS FROM DR. WILLINGHAM-TOURÉ

WEBINAR SLIDES

Can I Retire at 65?

WEBINAR OBJECTIVES

06-04-2025

-

Understand the 70-80% Rule - Is it for YOU?

-

Help you envision your unique retirement journey at 65.

-

Explore the personalized financial, psychological, social, and health considerations.

-

Provide tools and questions for your comprehensive planning.

-

Empower you to move from general concepts to personal action.

Click here to download your free presentation slides.

Retirement at 65: A Realistic Look from an African American Prospect

The aspiration to retire at 65 is a deeply held dream for many, symbolizing freedom, security, and a well-deserved rest after decades of work. However, for many African Americans, this traditional retirement age carries a unique set of considerations, challenges, and, importantly, strengths, shaped by historical and systemic factors that have profoundly impacted wealth accumulation and financial well-being.

While the general principles of retirement planning apply to everyone, understanding these specific dynamics is crucial for African Americans aiming for a secure retirement at 65 or any age.

The Stark Reality of the Racial Wealth Gap

The most significant factor impacting retirement readiness for many African Americans is the enduring racial wealth gap. Decades of systemic discrimination in housing, employment, education, and financial services have resulted in significant disparities in wealth accumulation:

-

Median Net Worth: In 2022, the median net worth of Black households was roughly six times lower than that of white households (around $44,100 compared to $284,310). This gap has remained stubbornly persistent for decades.

-

Retirement Account Ownership: African Americans are significantly less likely to have employer-sponsored retirement plans or IRAs. In 2022, only about 34.8% of Black families held retirement accounts, compared to 61.8% of non-Hispanic white families.

-

Lower Balances: Even when retirement accounts are held, median balances for African American savers are substantially lower across all income levels. For savers aged 51-64, Black households in the highest income third had median retirement savings roughly half that of white households in the same income bracket.

-

Income Disparities: Lower lifetime earnings, often due to wage inequality and higher rates of unemployment, directly impact the ability to save consistently and fully leverage employer matching programs.

These statistics paint a clear picture: retiring at 65 for many African Americans often means navigating retirement with fewer accumulated assets and a greater reliance on Social Security.

Unique Challenges in Retirement Planning

Beyond the wealth gap, several specific challenges often weigh more heavily on African American households as they approach retirement:

-

Caregiving Responsibilities: African Americans are disproportionately likely to be caregivers for aging parents, grandparents, or other family members. This often leads to reduced work hours, early retirement, or dipping into personal savings to cover care costs, significantly impacting their own retirement nest egg.

-

Health Disparities: Chronic illnesses, such as heart disease and diabetes, often occur at younger ages and with greater severity in the African American community. This can lead to higher out-of-pocket healthcare costs earlier in retirement and potentially shorter lifespans, impacting longevity planning.

-

Debt Burden: African American households, particularly graduates, tend to carry higher student loan debt and credit card balances, which can strain budgets and limit savings capacity throughout their working lives, extending into retirement.

-

Access to Financial Education & Advice: Historically, there have been barriers to culturally competent financial education and access to professional financial advisors, leading to less awareness of crucial planning strategies.

Strengths, Resilience, and Community

Despite these systemic challenges, the African American community possesses immense strength, resilience, and unique assets that can be leveraged for retirement planning:

-

Strong Family and Community Networks: These networks, while sometimes leading to increased caregiving responsibilities, also serve as powerful sources of support. Financial strategies can be built around family collective effort, shared resources, and mutual aid.

-

Entrepreneurial Spirit: A vibrant history of entrepreneurship within the Black community offers pathways for wealth creation that can extend into retirement, whether through small business ownership or consulting.

-

Emphasis on Generational Wealth: There's a growing awareness and drive within the community to build and transfer generational wealth, shifting focus from merely surviving to thriving and establishing a legacy.

-

Heightened Commitment to Financial Planning: Recent data suggests that Black households are increasingly proactive in their financial planning, committed to budgeting better, and more likely to create formal financial plans.

Crafting Your Retirement at 65: A Tailored Approach

For African Americans aspiring to retire at 65, the planning process requires a more strategic and intentional focus:

-

Aggressive Debt Elimination: Prioritize paying off high-interest debt (credit cards, personal loans) and aim to enter retirement mortgage-free if possible. Every dollar not spent on debt is a dollar that can be saved or invested.

-

Maximize Employer-Sponsored Plans: If available, contribute as much as possible to 401(k)s, especially to capture any employer match. Even small, consistent contributions compound significantly over time.

-

Leverage Roth Accounts: If eligible, consider Roth IRAs or Roth 401(k)s. Tax-free withdrawals in retirement can be invaluable, especially if you anticipate being in a higher tax bracket or want flexibility in managing your taxable income.

-

Strategic Social Security Claiming: Given a higher reliance on Social Security for retirement income, understanding your Full Retirement Age (FRA) and carefully considering the trade-offs of claiming early versus delaying benefits (potentially until 70) is paramount. This decision can significantly impact your lifetime income.

-

Early Investment & Diversification: Start investing as early as possible to take advantage of compounding. Diversify your investments beyond traditional retirement accounts, perhaps exploring real estate or business ventures that can provide additional income streams.

-

Comprehensive Healthcare Planning: Beyond Medicare, investigate Medigap policies, Medicare Advantage plans, and seriously consider long-term care insurance or alternative strategies for covering extended care costs.

-

Emergency Fund & Liquid Assets: Build a robust emergency fund (6-12 months of living expenses) to avoid having to tap into retirement savings prematurely during unexpected life events.

-

Professional Financial Guidance: Seek out a financial advisor who understands the unique financial realities and cultural nuances of the African American community. They can provide personalized strategies, help navigate complex decisions, and build trust. Look for Certified Financial Planners (CFPs) who prioritize a holistic approach.

-

Intergenerational Communication: Engage in open conversations with family members about financial planning, caregiving expectations, and estate planning to ensure everyone is on the same page and to avoid unintended financial burdens.

Conclusion

Retiring at 65 as an African American is a powerful goal that requires diligent planning and an acute awareness of both the systemic hurdles and the inherent strengths within the community. It's not just about accumulating a specific dollar amount; it's about building a robust financial foundation, fostering strong family and community networks, and embracing a holistic approach to well-being that ensures dignity, purpose, and peace of mind in your golden years. By confronting the realities head-on and leveraging every available resource, a fulfilling retirement at 65 can become a tangible reality.

Here's why "Mastering Your Money" is not just relevant, but essential:

-

Accelerating the Momentum: The 60% increase in median net worth for Black households is fantastic news, showing a clear trend towards financial improvement. A webinar like "Mastering Your Money" can act as a catalyst, providing the knowledge and tools to accelerate this positive momentum and empower individuals to build wealth even faster. It provides a structured path for those who are already on the right track or are eager to learn more.

-

Addressing the Persistent Wealth Gap: The fact that Black households still hold only $15 for every $100 of white household wealth underscores a deep-seated, systemic issue. While financial literacy alone isn't a "silver bullet" for closing this gap (historical and structural inequalities play a major role), it is a critical tool that empowers individuals to navigate and overcome some of these challenges within the existing system.

-

Strategic Decision-Making: Financial literacy equips individuals with the knowledge to make informed decisions about saving, investing, debt management, and wealth accumulation, which are all vital for closing wealth gaps.

-

Diversification of Assets: Data shows that Black wealth is often less diversified and relies heavily on home equity and vehicles, compared to white households which have greater proportional wealth in stocks and business assets. A webinar can introduce and demystify investing, encouraging diversification beyond traditional assets.

-

Avoiding Predatory Practices: Financial knowledge helps individuals identify and avoid predatory loans or financial products that disproportionately target vulnerable communities, thus preventing wealth erosion.

-

-

Building Generational Wealth: Financial literacy is foundational for building generational wealth. Understanding concepts like estate planning, smart investing, and intergenerational transfers can help Black families not just accumulate wealth for themselves but also pass it down to future generations, systematically reducing the gap over time.

-

Empowerment and Control: Money stress is a significant source of anxiety. Providing practical knowledge and actionable steps empowers individuals to take control of their financial lives, fostering a sense of agency and reducing stress. This is particularly important for communities that have historically faced systemic economic disadvantages.

-

Leveraging Economic Trends: The increase in Black household wealth from 2019-2022 was largely driven by rising home equity and, to some extent, an increase in business assets. A financial literacy webinar can help individuals understand how to leverage these trends strategically, for example, by teaching them how to build equity, manage mortgages effectively, or scale small businesses.

-

Filling Knowledge Gaps: Research consistently shows that financial literacy levels vary across demographics, and minority groups, even those with higher education, may face unique challenges due to structural barriers. A webinar specifically designed to be accessible and relevant can help fill these knowledge gaps and provide targeted guidance.

In essence, "Mastering Your Money" serves as a vital educational resource that can empower Black households to:

-

Capitalize on existing positive trends.

-

Strategically navigate financial systems.

-

Build more diversified and resilient wealth.

-

Accelerate progress toward closing the persistent wealth gap, moving closer to true financial freedom and equity.

WEBINAR OBJECTIVES

05-28-2025

By the end of this session, you will be able to:

-

Understand core budgeting principles.

-

Differentiate between good and bad debt.

-

Recognize basic investing concepts.

-

Identify strategies for saving and growing your money.

-

Take actionable steps towards financial well-being.

Download your free presentation slides here

Mastering Your Money 101

Black households are making significant strides in increasing their median net worth (a 60% increase from 2019 to 2022, the largest of any racial group). However, a substantial wealth gap still exists (Black households held only $15 for every $100 held by white households in 2022).

This disparity, despite the impressive gains, is precisely why this webinar matters so profoundly, especially for the Black community.

Here's why "Mastering Your Money" is not just relevant, but essential:

-

Accelerating the Momentum: The 60% increase in median net worth for Black households is fantastic news, showing a clear trend towards financial improvement. A webinar like "Mastering Your Money" can act as a catalyst, providing the knowledge and tools to accelerate this positive momentum and empower individuals to build wealth even faster. It provides a structured path for those who are already on the right track or are eager to learn more.

-

Addressing the Persistent Wealth Gap: The fact that Black households still hold only $15 for every $100 of white household wealth underscores a deep-seated, systemic issue. While financial literacy alone isn't a "silver bullet" for closing this gap (historical and structural inequalities play a major role), it is a critical tool that empowers individuals to navigate and overcome some of these challenges within the existing system.

-

Strategic Decision-Making: Financial literacy equips individuals with the knowledge to make informed decisions about saving, investing, debt management, and wealth accumulation, which are all vital for closing wealth gaps.

-

Diversification of Assets: Data shows that Black wealth is often less diversified and relies heavily on home equity and vehicles, compared to white households which have greater proportional wealth in stocks and business assets. A webinar can introduce and demystify investing, encouraging diversification beyond traditional assets.

-

Avoiding Predatory Practices: Financial knowledge helps individuals identify and avoid predatory loans or financial products that disproportionately target vulnerable communities, thus preventing wealth erosion.

-

-

Building Generational Wealth: Financial literacy is foundational for building generational wealth. Understanding concepts like estate planning, smart investing, and intergenerational transfers can help Black families not just accumulate wealth for themselves but also pass it down to future generations, systematically reducing the gap over time.

-

Empowerment and Control: Money stress is a significant source of anxiety. Providing practical knowledge and actionable steps empowers individuals to take control of their financial lives, fostering a sense of agency and reducing stress. This is particularly important for communities that have historically faced systemic economic disadvantages.

-

Leveraging Economic Trends: The increase in Black household wealth from 2019-2022 was largely driven by rising home equity and, to some extent, an increase in business assets. A financial literacy webinar can help individuals understand how to leverage these trends strategically, for example, by teaching them how to build equity, manage mortgages effectively, or scale small businesses.

-

Filling Knowledge Gaps: Research consistently shows that financial literacy levels vary across demographics, and minority groups, even those with higher education, may face unique challenges due to structural barriers. A webinar specifically designed to be accessible and relevant can help fill these knowledge gaps and provide targeted guidance.

In essence, "Mastering Your Money" serves as a vital educational resource that can empower Black households to:

-

Capitalize on existing positive trends.

-

Strategically navigate financial systems.

-

Build more diversified and resilient wealth.

-

Accelerate progress toward closing the persistent wealth gap, moving closer to true financial freedom and equity.

WEBINAR OBJECTIVES

05-28-2025

By the end of this session, you will be able to:

-

Understand core budgeting principles.

-

Differentiate between good and bad debt.

-

Recognize basic investing concepts.

-

Identify strategies for saving and growing your money.

-

Take actionable steps towards financial well-being.

Download your free presentation slides here